FRTB

WHAT IS THIS? The Fundamental Review of the Trading Book (FRTB) is a set of market risk capital rules designed to replace a series of patches introduced after the financial crisis. It seeks to better-capture tail risk, to redraw the boundary between banking and trading books, and to raise the bar for internal models.

Blueprint for FRTB: Building a future-state business strategy

Sponsored feature: Numerix

SGX risk chief urges Asia lobbying push on FRTB

Asian markets could be stifled by “irrelevant” global standards, warns Koh

FRTB data pooling crawls into action

Dealers voice concerns on data pooling as industry initiative to model risk factors faces significant challenges

Taking the FRTB plunge

Banks entering chilly FRTB waters for first time facing fresh challenges

FRTB sends banks around the bend

Banks uncover hidden challenges of data, computing power and need for joined-up approach

FRTB: a work in progress

Banks cannot wait for clarification but must forge ahead

Lining up the fundamentals

Sponsored Q&A: Asset Control, Murex, Vector Risk, CompatibL, Parker Fitzgerald and Numerix

Regulations, sensitivities and adjoints: Using AAD for FRTB and FRTB-CVA

Sponsored feature: CompatibL

Attribution of risk measures for improved risk and capital control

Sponsored feature: GFT

Freeing up the front office

Sponsored feature: Parker Fitzgerald

The decentralisation trap: The FRTB standardised approach

Sponsored feature: Vector Risk

Land of confusion: FRTB and the calculation burden

Sponsored feature: Quaternion Risk Management

No way out: The road to FRTB compliance

Sponsored feature: Murex

Deutsches Risk Rankings 2016

Derivatives dealers offer simplicity as regulatory change continues apace

Banks plan risk factor exclusion to avoid FRTB surcharge

Firms hope to leave out non-modellable risk factors deemed "immaterial"

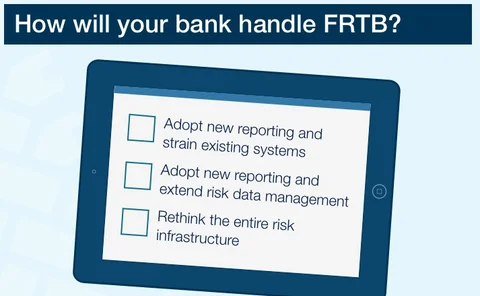

FRTB: Is your bank on track?

Content provided by IBM

FRTB standard rules cause worries about duplication

Sensitivity-based approach means “we have to do everything twice”, complains one head of trading

Banks fear costs from loss of AAD under simpler FRTB rules

Trading book regime may force use of more expensive and time-consuming ways of computing risk sensitivities

The P&L attribution mess

FRTB model approval regime dogged by confusion and controversy

Banks fear FRTB internal model approval gridlock

UK regulator said to have concerns about the high volume of simultaneous approval requests

Details of vital FRTB model test still up for grabs

Banks argue valuation adjustments should be left out of the model approval process

The growing pull of public cloud for banks and regulators

Adoption by the FCA for Mifid II data reporting indicates public cloud satisfies regulatory, security and reliability requirements

Futureproofing risk management

Sponsored Q&A: Numerix

Structured products: The new value chain

Sponsored Q&A: Murex