Residential mortgage-backed securities (RMBSs)

Market graphic - A consensus for valuation input assumptions

Money managers' expectations for the 12-month performance of underlying loans behind European RMBS are showing signs of improvement, says Peter Jones

UK guarantees AAA RMBS in bid to jump-start lending

The UK government has launched a scheme to guarantee up to £50 billion in residential mortgage-backed securities (RMBS) for the first time, finance minister Alistair Darling said yesterday.

S&P: AAA RMBS writedowns will be minimal

AAA rated tranches of US subprime residential mortgage-backed securities (RMBS) will be written down by less than 1%, despite heavy losses on the underlying mortgages, rating agency Standard & Poor's predicts.

Gathering confidence

Securitisation

Jump-start needed

Securitisation

Dearth of direction

Editor's letter

Rating agencies conflicts of interests revealed in SEC report

Daily news headlines

Call of duty

Government-sponsored Enterprises

BoE reveals £50bn liquidity facility

Banks have welcomed a scheme by the Bank of England (BoE) aimed at improving the balance sheets of UK financial institutions. The £50 billion facility, announced on April 21, will allow financial institutions to swap illiquid mortgage-backed securities…

Offshore insecurity

Securitisation

One-way fear

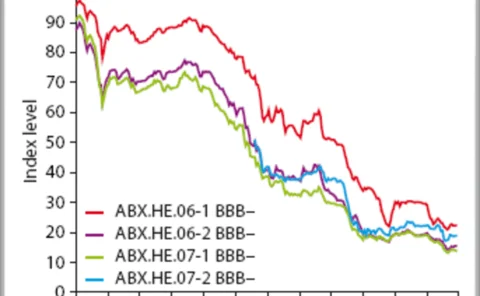

ABX Index