Implied volatility

Volatility has become affordable again, says Deutsche Bank

Volatility has become affordable again, says Deutsche Bank

Sponsored statement: Royal Bank of Scotland

Yield enhancement on Asian equity indexes through call overwriting

Derivatives research house of the year: Deutsche Bank

Risk awards 2011

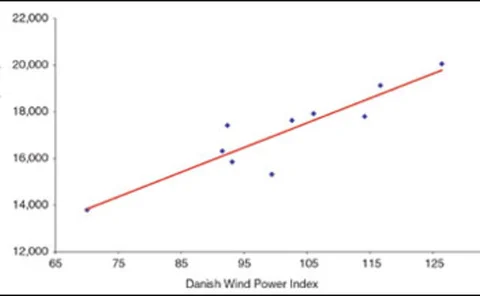

Hong Kong to get volatility index ‘early next year’

Hong Kong will get a real-time VIX index in the first quarter next year, according to Hang Seng Indexes.

Curbing dispersion exposure

Dispersion tactics

A Libor market model with a stochastic basis

A Libor market model with a stochastic basis

Barclays Capital’s VXX is bleeding volatility, analysts claim

An upwardly sloping term structure of volatility is dragging on the performance of the popular exchange-traded note.

Eurostoxx 50 investors 'unintentionally making a bet on financials', according to research

Tobam's analysis of financial markets diversification suggests that eurozone indexes might not be as diversified as investors believe

Sponsored statement: Using options to improve portfolio risk/returns

Using options to improve portfolio risk/returns

Equity derivatives

Equity derivatives special report

Equity investors struggle with high correlation

Dealing with a break-up

End-users rush into hedging oil prices

End-users are ploughing into hedging their oil positions, as prices remain in a tight range, says Standard Chartered Bank’s head of energy and environmental research

Structural shifts in equity flows and ETFs force up correlation, says HSBC

HSBC's global report indicates that correlation in the global equities market has been steadily rising since 2001.

Sponsored statement: Controlling volatility to reduce uncertainty

Controlling volatility to reduce uncertainty

A dynamic model for correlation

Equity markets have experienced a significant increase in correlation during the crisis, resulting in exotic derivatives portfolios realising large losses. As larger correlations in downward scenarios are already implied in the index option market in the…

Putting the smile back on the face of derivatives

Cross-asset quadratic Gaussian models have been limited in the scale of their implementation by the difficulty in ensuring the correct drift conditions to omit arbitrage. Here, Paul McCloud shows how to exploit the symmetries of the functional form to…

Smile dynamics IV

Lorenzo Bergomi addresses the relationship between the smile that stochastic volatility models produce and the dynamics they generate for implied volatilities. He introduces a new quantity, the skew stickiness ratio (SSR), and shows how, at order one in…

Sponsored statement: The implied volatility surface in the presence of dividends

Standard Bank quantitative analyst Roelof Sheppard shows how absolute and proportional dividend payments give rise to arbitrage constraints on the implied volatility surface

Combining the SABR and LMM models

Pierre Henry-Labordere analyses a stochastic volatility Libor market model that combines the SABR and Brace-Gatarek-Musiela (BGM) models in a natural way. Using an innovative geometrical method, he explains how to obtain analytical formulas for swaption…

The equity volatility-credit link

Sponsored Statement

Combining the SABR and LMM models

Pierre Henry-Labordere analyses a stochastic volatility Libor market model that combines the SABR and Brace-Gatarek-Musiela (BGM) models in a natural way