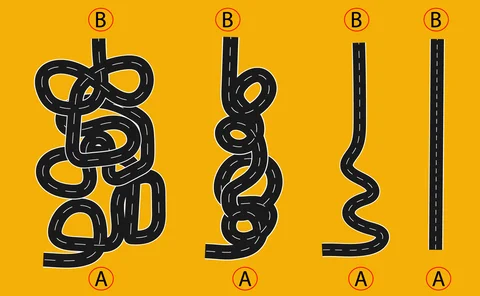

Correlation

Collapse of correlation fails to stem zeal for dispersion

New analysis suggests immensely popular relative value strategy may have more upside

‘Fear gauge’ within expectations, some say

Several options specialists dismiss claims that structured products are distorting the Vix

Quants are using language models to map what causes what

GPT-4 does a surprisingly good job of separating causation from correlation

Infrequent MtM reduces neither value-at-risk nor backtesting exceptions

Frequency of repricing impacts volatility and correlation measures

Estimating the correlation between operational risk loss categories over different time horizons

The authors propose and demonstrate the value of a model with which mathematical techniques can be applied to analytically calculate means, variances and covariances more accurately than Monte Carlo simulations.

What have we learned from 20 million historical US stock data?

The author offers a statistical characterization of the US stock market from January 3, 1995 to June 11, 2021.

Equitable lobbies for concentration charge on riskier ABS

“Ultra-high correlation of losses” between lower-rated tranches requires new regulation, insurer says

Smile-consistent basket skew

An analytic approximation for the implied volatility surface of basket options is introduced

Commerz’s market RWAs up 9% on EBA technical update

Updated list of closely correlated currencies removes lower fund requirements from 197 pairs

How banks can avoid bad haircuts on hedge fund trades

HSBC quant makes case for looking at collateral and funding rates in concert

How Man Numeric found SVB red flags in credit data

Network analysis helps quant shop spot concentration and contagion risks

‘Spectacular’ vol disconnect ‘ominous’ for risk assets

Historic divergence has caught the eye of Boaz Weinstein and others

‘Globalisation rewired’: what does it mean for investors?

After half a century of outsourcing production to developing nations, companies are changing tack – with long-term implications for investors

Concern over sluggish adoption of ESG futures

While the number of products is on the rise, very few have underlying liquidity

Keep risk parity simple, stupid

In times of volatility, simpler risk parity strategies may outperform more elaborate counterparts

Talking Heads 2022: Rates market ruckus

Inaugural interview series looks at how sell-side traders are adapting to a world of surging inflation and rates

No link between geopolitical risk signals and returns – hedge fund

Gauges of geopolitical risk are better at predicting volatility than equity returns, research from XAI finds

Data-driven wrong-way risk

A calculation method for regulatory CVA wrong-way risk based on credit and exposure is introduced

Barclays confronts ‘implausible’ macro risks

Talking Heads 2022: Bank is reaping rewards of sticking with its trading businesses, says macro head Lublinsky

How Citi is handling topsy-turvy rates markets

Talking Heads 2022: Rate hikes and inflation have forced a rethink of the US bank’s hedging strategies

Using correlation to model op risk losses may be unsafe – study

Techniques for linking economic factors and bank losses produce varying – and sometimes contradictory – results

How a credit run affects asset correlation

This paper analyzes how soaring demand in the lending market shortly before a financial crisis can affect one of the main parameters in the internal ratings-based approach: the asset correlation.

Rates correlations break down amid volatility surge

Dealers say go-to hedges are now too risky as old relationships fail

Correlations in operational risk stress testing: use and abuse

The paper presents an analysis of correlation effects of economic factors on the operational risk losses of a medium-large UK retail bank, and it recommends that causal factors that effect operational risk should be identified.