Monthly swaps data review: volumes rise, CCP switches spike

In the first of a new series of articles, Amir Khwaja of Clarus FT looks at the most recent batch of swaps data

There are more sources of over-the-counter derivatives data available today than at any point in the market’s history. In this series of monthly articles, Amir Khwaja, chief executive of Clarus Financial Technology, looks for trends.

This month, the increase in US interest rates appears to have kicked off a burst of swaps activity, and there has been a surge in central counterparty (CCP) switch trades, allowing dealers to manage their margin requirements at the market’s largest two rates clearing houses.

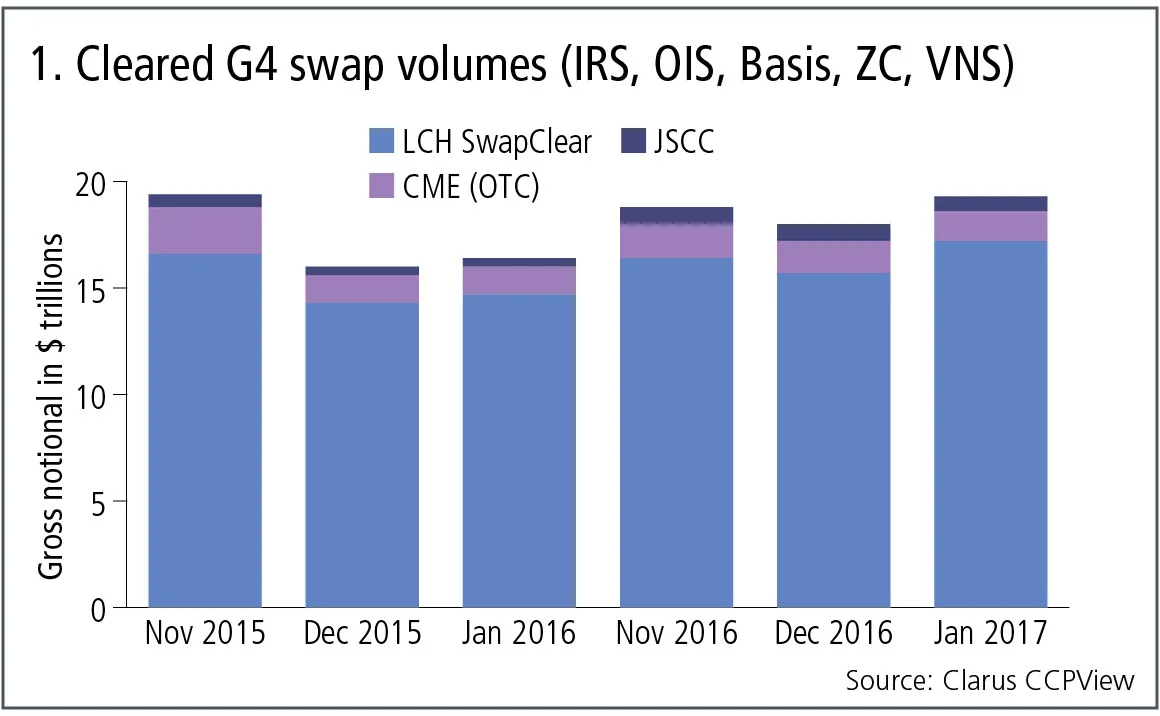

Global cleared volumes

Interest rate swaps are the largest product in gross notional terms, so let’s start with monthly volumes in the G4 currencies (euro, sterling, US dollar, yen) of global cleared swaps and compare each of the three most recent months with their corresponding months a year earlier (see figure 1). The numbers below are single-counted, meaning a swap transacted between two counterparties is counted once, as opposed to the double-count in use by many clearing houses.

Figure 1 shows:

• LCH has the largest cleared volume, with $17.2 trillion in January 2017.

• CME has $1.4 trillion and the Japan Securities Clearing Corporation has $0.7 trillion.

• Eurex and Spain’s Bolsas y Mercados Españoles also have volume, but it is negligible in comparison.

• A total of $19.3 trillion was cleared in January 2017, for a year-on-year increase of 18%.

• January 2017 is up from December 2016, which itself was 13% up from December 2015.

• Cumulative volume for the most recent two months is 15% above the same period a year earlier and a strong indication of higher levels of hedging and trading activity as US interest rates start to rise.

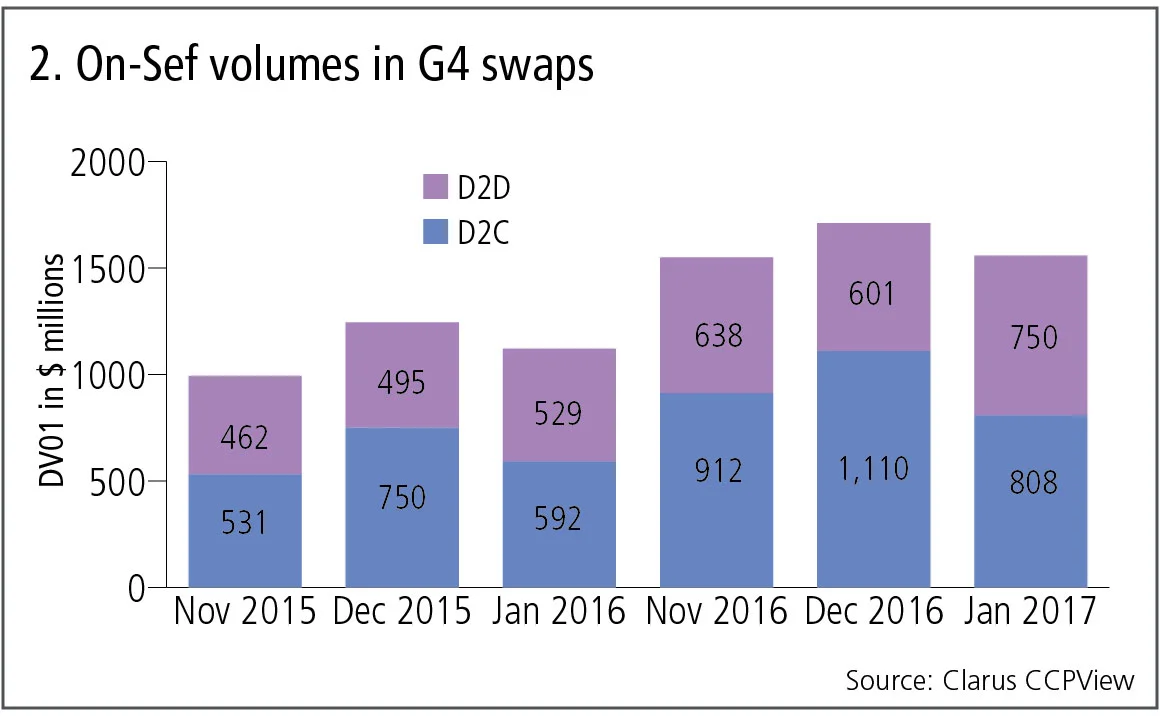

Swap execution facilities

Swap execution facilities (Sefs) are trading venues mandated for a subset of the cleared swaps executed by US-regulated market participants and are required to publish daily volumes.

For the same G4-currency swaps, the gross notional reported by Sefs in January 2017 is $3.7 trillion, which represents 19% of the $19.3 trillion in total cleared volume – or roughly a fifth (see figure 2). This might not seem large, but it represents a good chunk of global liquidity when considering the products not subject to the Sef mandate: forward-starting swaps are predominantly traded off-Sef, non-US dollar currency volume is traded in Europe or Japan, and products such as overnight indexed swaps (OIS), basis swaps, zero-coupon swaps and variable notional swaps are predominantly executed off-Sef.

Figure 2 shows:

• Rising volumes compared with a year earlier.

• January 2017 is up 39% year on year, while December 2016 is up 37% and November 2016 is up 56%.

• This reflects both growth in trading volumes and in the proportion executed on-Sef.

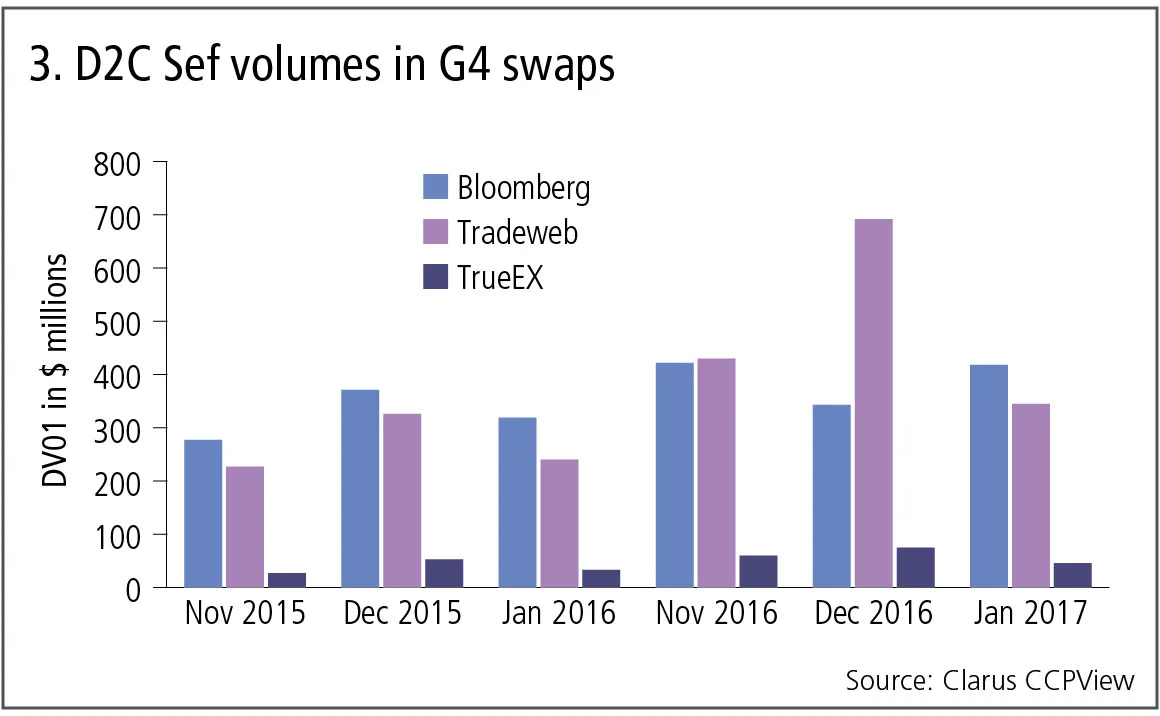

D2C and D2D Sefs

Sefs are required by US regulation to provide access to all market participants but, in practice, trading between dealers and clients is generally conducted on one group of venues, using the request-for-quote protocol that resembles traditional voice trading, while inter-dealer generally trading takes place on a second group (see figures 3 and 4).

In each month, dealer-to-client volumes are higher than volumes between dealers, sometimes significantly so. Generally, Bloomberg and Tradeweb, the leading dealer-to-client Sefs, are transacting larger risk volume than the leading interdealer Sefs – Icap, Tradition and Tullett Prebon – and there must be meaningful differentiation and specialisation between the eight platforms for all to operate successfully.

Tullett’s acquisition of the voice-broking business of rival Icap also included the latter’s interdealer Sef, i-Swap. The new firm, TP Icap, now owns two Sefs and more than 50% of overall interdealer trading if it can hang onto the volumes on each. It is not known whether TP Icap plans to consolidate the two platforms or continue running them in parallel.

Figure 3 shows:

• Bloomberg and Tradeweb vying each month for the lead.

• Bloomberg was ahead in each of the first three, but Tradeweb had the edge in November and December 2016.

• Tradeweb recorded a huge month in December 2016, driven by record volumes of compression list trading (in which dealers quote prices for offsetting trades, which can later be netted against a participant’s existing positions).

• TrueEX is the only remaining start-up Sef in rates swaps, also with good compression list volumes.

Figure 4 shows:

• Volume is split between five Sefs.

• Icap the largest, with Tradition and Tullett Prebon close.

• BGC and Dealerweb are further behind.

• Volumes are up at each of these five Sefs.

Swap data repositories (SDRs)

In the US, the Commodity Futures Trading Commission requires over-the-counter derivatives transactions to be publicly disseminated by SDRs and this trade-level data provides more insight into the market.

This data does have to be used carefully as larger trades do not have their full notional disclosed, in order that market-makers have a chance to hedge after the trade has been executed. Nevertheless, it still provides a unique insight into trading activity.

As one example, the data can be used to show that off-Sef cleared gross notional volume is as large as on-Sef cleared volume.

This suggests that as well as the $3.7 trillion of on-Sef gross notional, there is a similar amount off-Sef and cleared, giving a total of $7.4 trillion in January 2017 for the US market as a whole in these G4-currency swaps.

This represents 38% of the global cleared figure of $19.3 trillion and is in line with intuition, as we expect US dollar swaps to be 35–40% of global volume. While some US dollar swaps will trade outside the US, the majority trade in the US. Similarly, the vast majority of sterling, euro and yen swaps trade in Europe and Japan.

Further in January 2017, a total of 50,000 cleared G4 swaps trades were reported to US SDRs, of which 90% were interest rate swaps, 6% OIS and 4% basis. As a rule of thumb, the US market in G4 swaps is around 2,500 trades a day with an average notional per trade of $150 million.

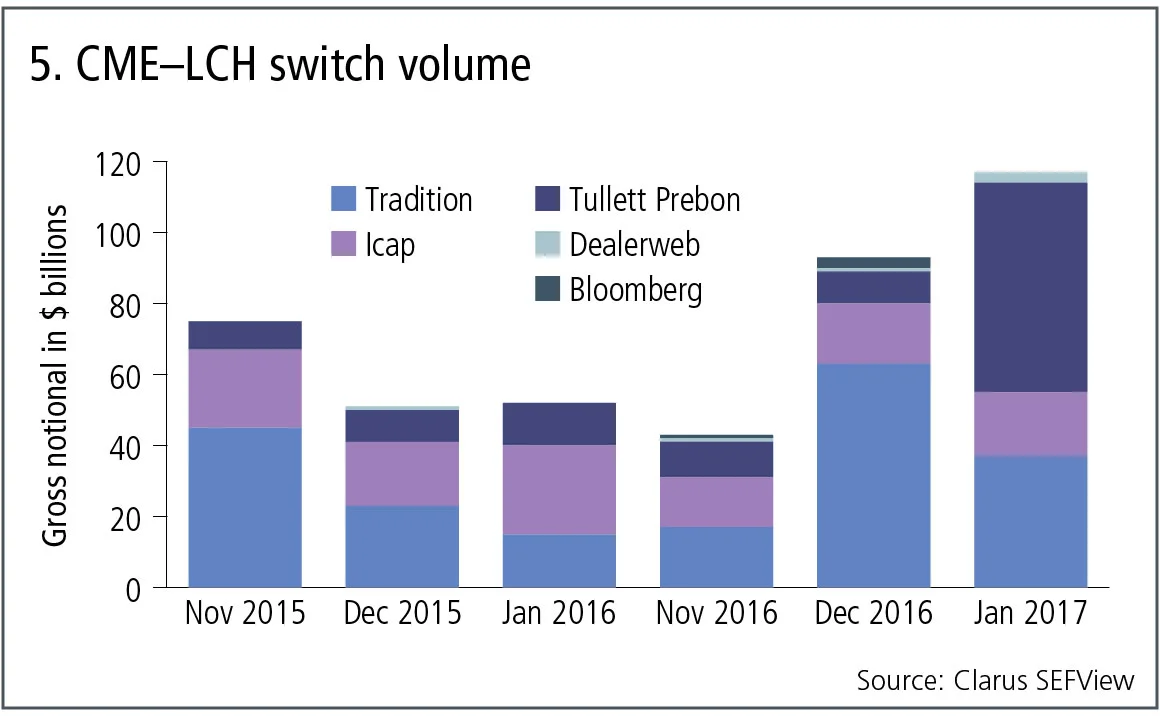

CCP switch trades

A recent market development has been the emergence of a basis spread between swaps cleared at LCH and those cleared at CME. This led to the broking of CCP ‘switch trade’ activity, in which swap dealers agree to simultaneously pay fixed at one CCP and receive fixed at the other, with another dealer taking the opposite view (see figure 5).

Figure 5 shows:

• Volume has been higher in the recent two months, at $93 billion and $116 billion.

• In fact, both are record highs since the inception of this market in early 2015.

• Tradition has the largest share in most months, followed by Icap.

• January 2017 shows a massive jump at Tullett due to huge two-year volume, unusual for this tenor where the basis is only 0.15 basis points compared to 3.3bp for five-year.

Only users who have a paid subscription or are part of a corporate subscription are able to print or copy content.

To access these options, along with all other subscription benefits, please contact info@risk.net or view our subscription options here: http://subscriptions.risk.net/subscribe

You are currently unable to print this content. Please contact info@risk.net to find out more.

You are currently unable to copy this content. Please contact info@risk.net to find out more.

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@risk.net

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@risk.net

More on Markets

Leveraged ETFs may have fuelled Kospi plunge

Record one-day drop in Korean equity markets follows months-long surge driven by levered bets

Iran conflict forces EM carry trade unwinds

Surging oil prices, rising vol and dollar flight triggered stop-outs of emerging market positions, say dealers

Eurex mulls ‘integrated’ prediction market

Dividend derivatives seen as template for event contract expansion

After market whipsaws, banks put new twist on QIS options

Variable strike options aim to catch recoveries after volatility spikes

Broker quoting gap keeps Eurex-LCH basis alive

Lack of differentiated prices helps retain CCP basis

QIS futures debut – but only simple ones for now

Goldman and Societe Generale kick-start Eurex market with equity baskets

Hedge funds trim US swap spreads on tariff decision

Investors cut back asset swap positions as Supreme Court ruling reignites deficit concerns

Opinions split on EU bond balance sheet squeeze

Some say QT and issuance wave will hamper intermediation; others say dealers nimble enough to respond